")

The year 2026 represents a profound structural and aesthetic inflection point for the wearable technology sector in India. Having aggressively transitioned from a nascent market of peripheral smartphone accessories to a cornerstone of personal computing and health telemetry, the industry is currently undergoing a complete metamorphosis.

This transition, categorized within industry parlance as “Wearables 2.0”, is characterized by the invisible integration of advanced biometric sensors, edge artificial intelligence (AI) algorithms, and state-of-the-art material science into traditional apparel, smart jewelry, hearables, and eyewear.

Concurrently, the macroeconomic and regulatory landscape of the Indian wearables market is undergoing a fundamental realignment. Following a prolonged period of hyper-growth heavily driven by the commoditization of entry-level smartwatches, the market has experienced a significant volume correction. Modern Indian consumers are actively rejecting basic step-counters in favor of medical-grade biometric accuracy, vernacular AI interfaces, and premium build quality.

This The Knowledge Company Perspective analysis provides an exhaustive, multi-disciplinary analysis of the technological, economic, and cultural forces shaping the Indian wearable market today.

To fully contextualize the ongoing fashion-technology convergence in India, it is imperative to dissect the overarching economic indicators dictating vendor strategies. The Indian wearable technology market is navigating a complex period of quantitative consolidation paired with massive qualitative premiumization.

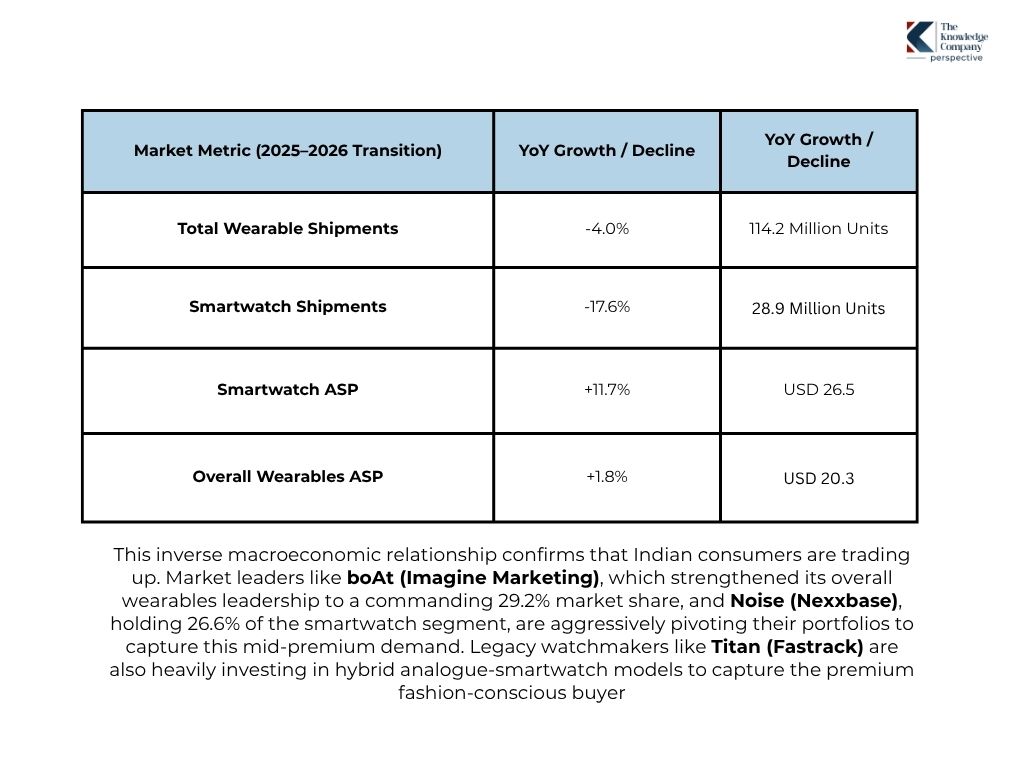

According to recent IDC data closing out 2025, India’s overall wearable device market fell by 4.0% year-over-year (YoY) to 114.2 million units. This downturn was driven almost entirely by the smartwatch category, which saw shipments fall 17.6% YoY to 28.9 million units.

However, analytical models prove this contraction is not indicative of a failing market, but rather a symptom of “demand fatigue” within the hyper-commoditized, sub-premium segment. Consumers are holding out for meaningful upgrades. As proof of this premiumization, the Average Selling Price (ASP) has surged.

2. Hearables & The Audio AI Renaissance: The Shift to Premiumization

While smartwatches faced a severe volume correction, the earwear category (Truly Wireless Stereo or TWS) continues to act as the undeniable backbone of the Indian wearables market, accounting for over 70% of total unit shipments.

However, the 2026 hearables market is defined by a fascinating paradox: declining volume but surging revenue. First-time urban buyers have saturated the market, leading to a slight volume dip. Yet, overall category revenue has climbed as Indian consumers pivot aggressively toward premiumization and replacement upgrades, forcing brands across every price tier to completely overhaul their audio architectures.

The battleground is no longer dictated by basic battery life; it is entirely driven by Spatial Audio, Edge AI, and form-factor innovation across three distinct market tiers:

To capture the massive influx of consumers from Tier 2 and Tier 3 cities, the sub-₹2,000 segment aggressively democratizes technology. Homegrown titans like boAt, Noise, Mivi, and Boult are pushing feature-rich TWS devices offering 50-hour playtimes and AI-based Environmental Noise Cancellation (ENC) as baseline expectations.

Meanwhile, the ₹2,001–₹5,000 segment acts as a critical “innovation bridge.” Smartphone-led ecosystem brands like Nothing (CMF)—which recently recorded a staggering 91.5% YoY growth—and OnePlus dominate this tier. They are coercing budget buyers into higher spending by offering selective premium features, such as case haptics, multi-device multipoint connectivity, and entry-level spatial audio.

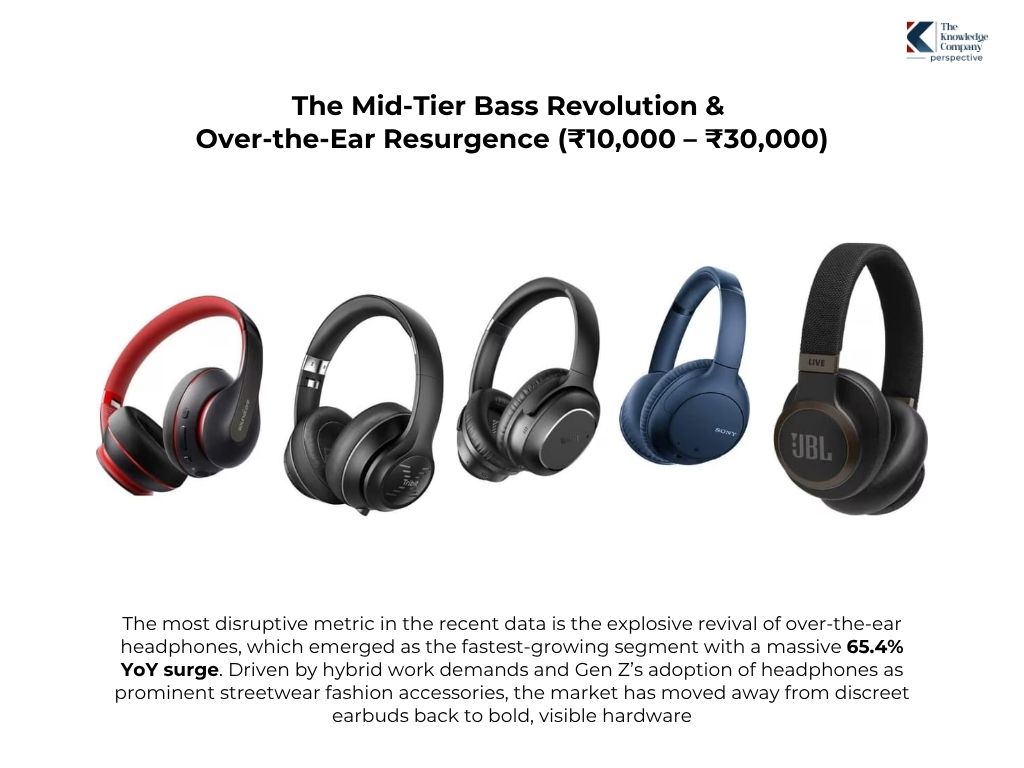

The most disruptive metric in the recent data is the explosive revival of over-the-ear headphones, which emerged as the fastest-growing segment with a massive 65.4% YoY surge. Driven by hybrid work demands and Gen Z’s adoption of headphones as prominent streetwear fashion accessories, the market has moved away from discreet earbuds back to bold, visible hardware.

In this tier, Sony has masterfully captured the Indian youth market with its ULT WEAR (WH-ULT900N) series (priced around ₹14,990). Recognizing the Indian affinity for heavy bass, the ULT series features dedicated “ULT1 and ULT2” listening modes that physically boost low frequencies on demand. Paired with brands like Sennheiser (Accentum) and Samsung (JBL), this tier brings advanced ANC and Dolby Atmos head-tracking to the masses.

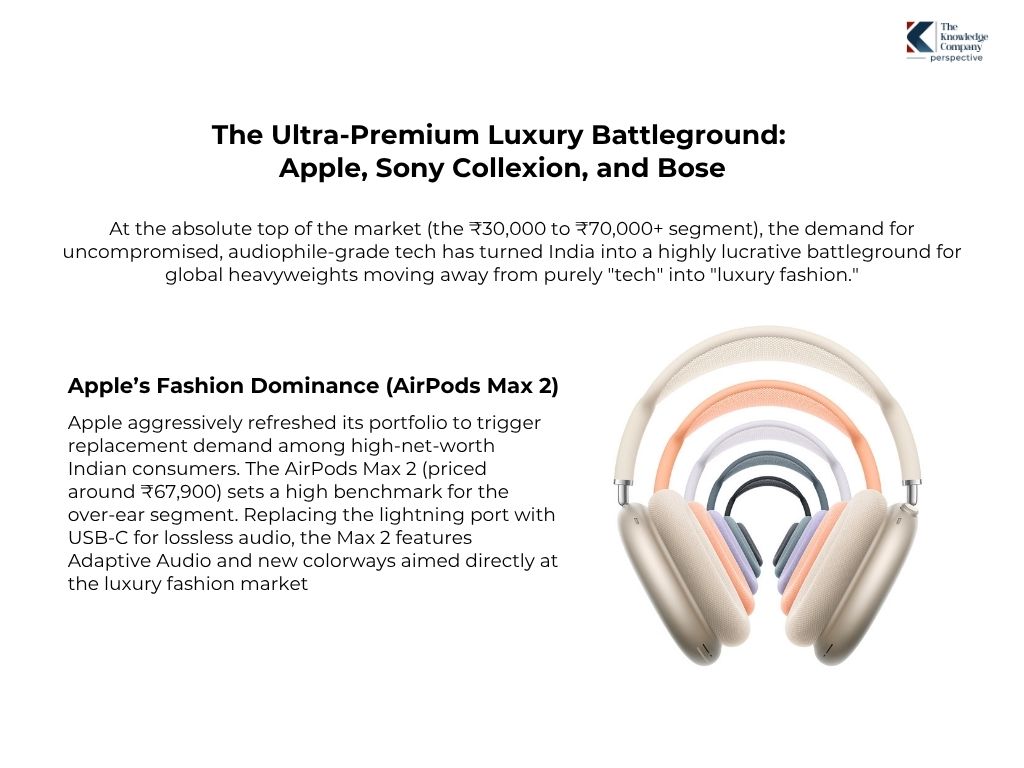

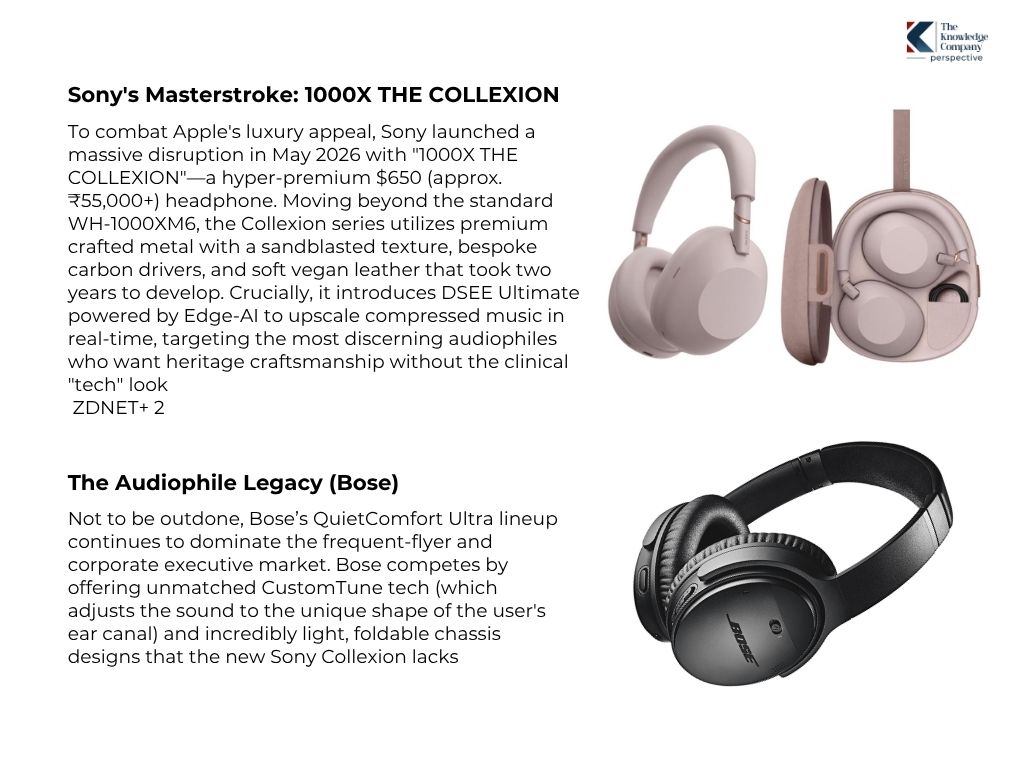

At the absolute top of the market (the ₹30,000 to ₹70,000+ segment), the demand for uncompromised, audiophile-grade tech has turned India into a highly lucrative battleground for global heavyweights moving away from purely “tech” into “luxury fashion.”

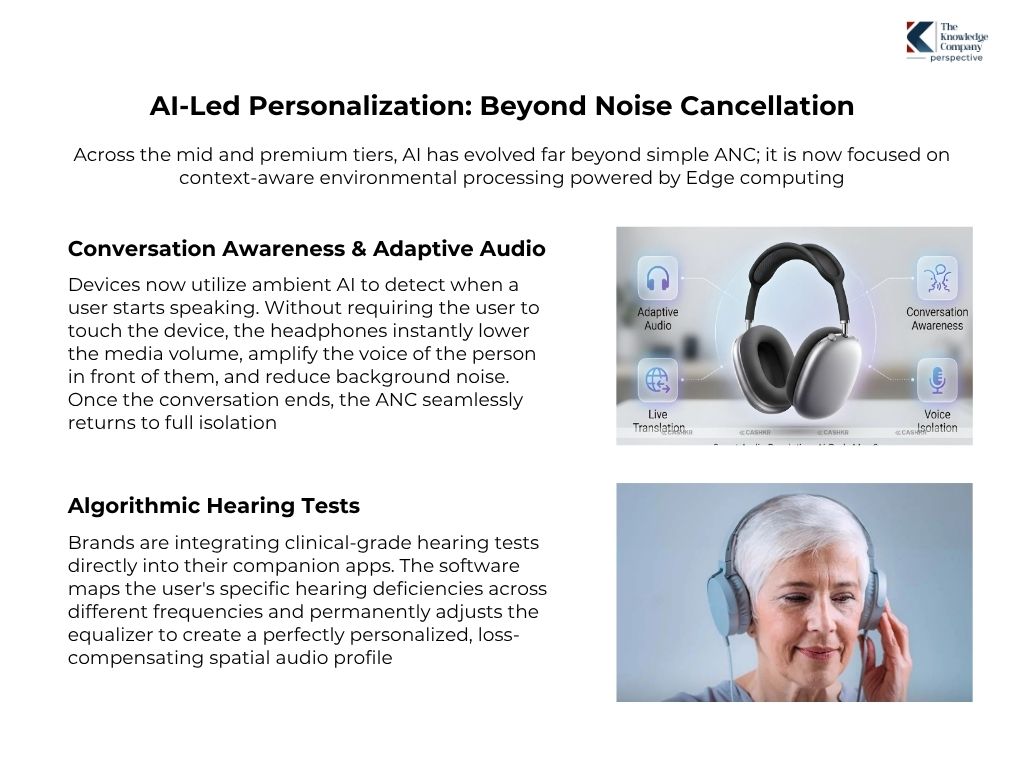

Across the mid and premium tiers, AI has evolved far beyond simple ANC; it is now focused on context-aware environmental processing powered by Edge computing.

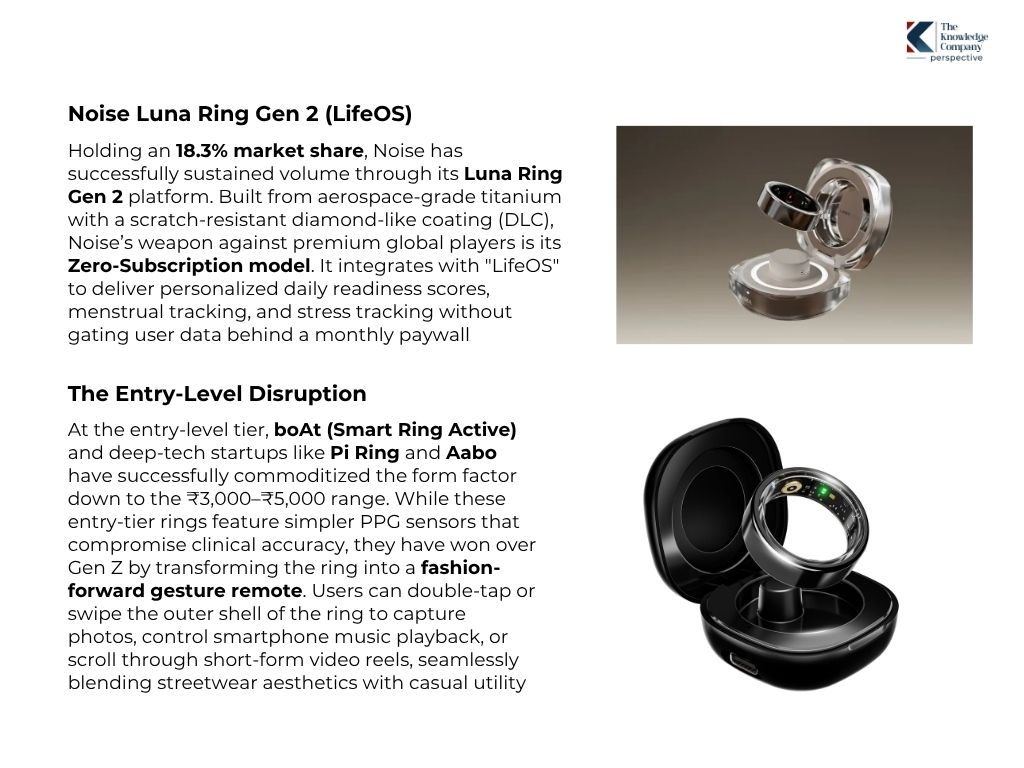

In 2026, the smart ring has evolved from an experimental niche product into a primary force disrupting the broader consumer electronics market, systematically capturing market share from traditional wrist-worn fitness trackers. By entirely removing the distraction of a screen, smart rings focus on “ambient bio-intelligence”—silently, passively collecting clean data from the finger’s capillaries where arterial blood flow yields significantly more accurate biometric readings than the wrist.

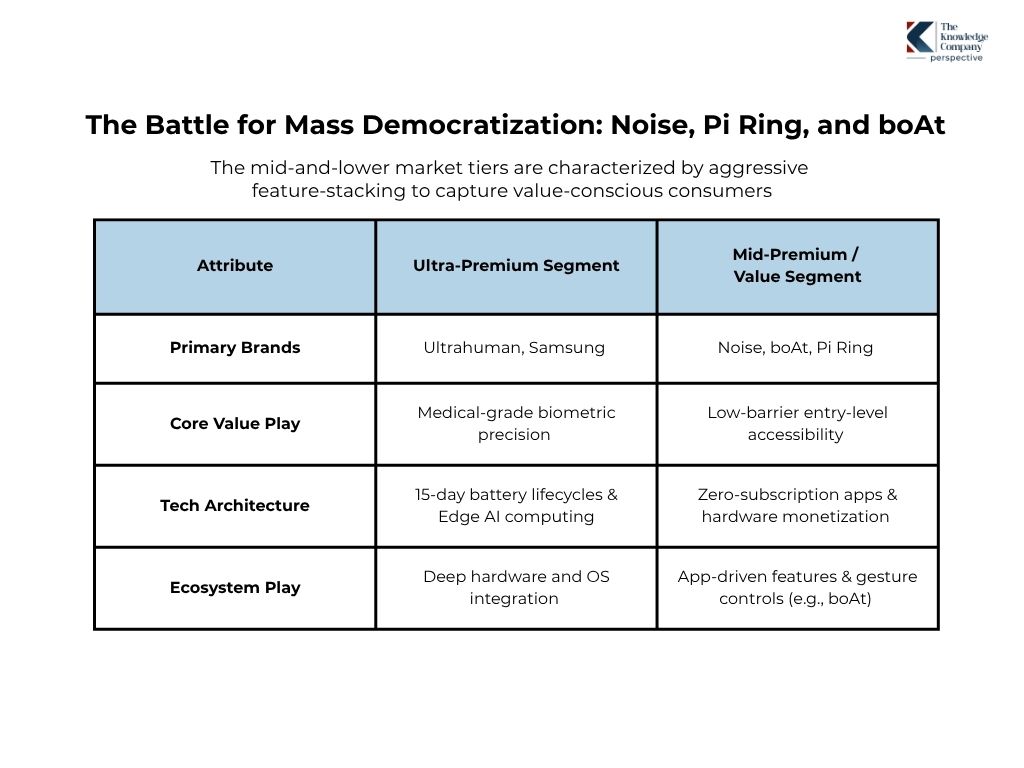

The Indian smart ring market has matured into a fiercely contested, multi-tiered ecosystem where homegrown pioneers are successfully holding off global tech conglomerates through localized software ecosystems and subscription-free ownership models.

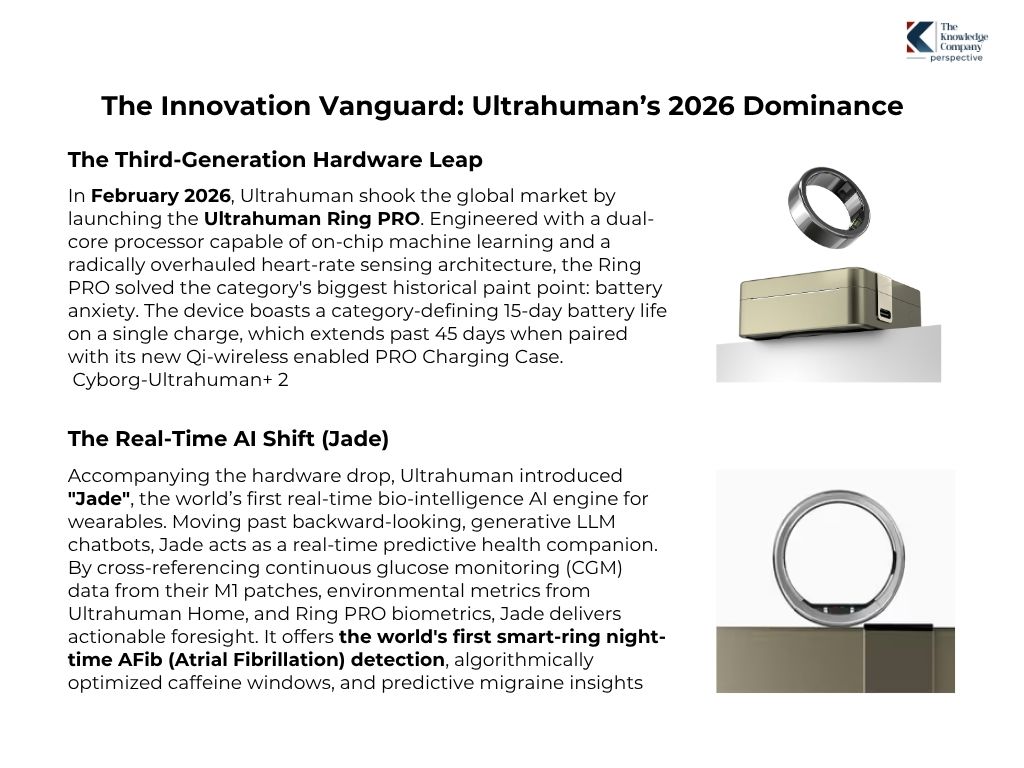

Homegrown health-tech titan Ultrahuman controls a commanding 30.4% market share in India, acting as the definitive benchmark for the premium category.

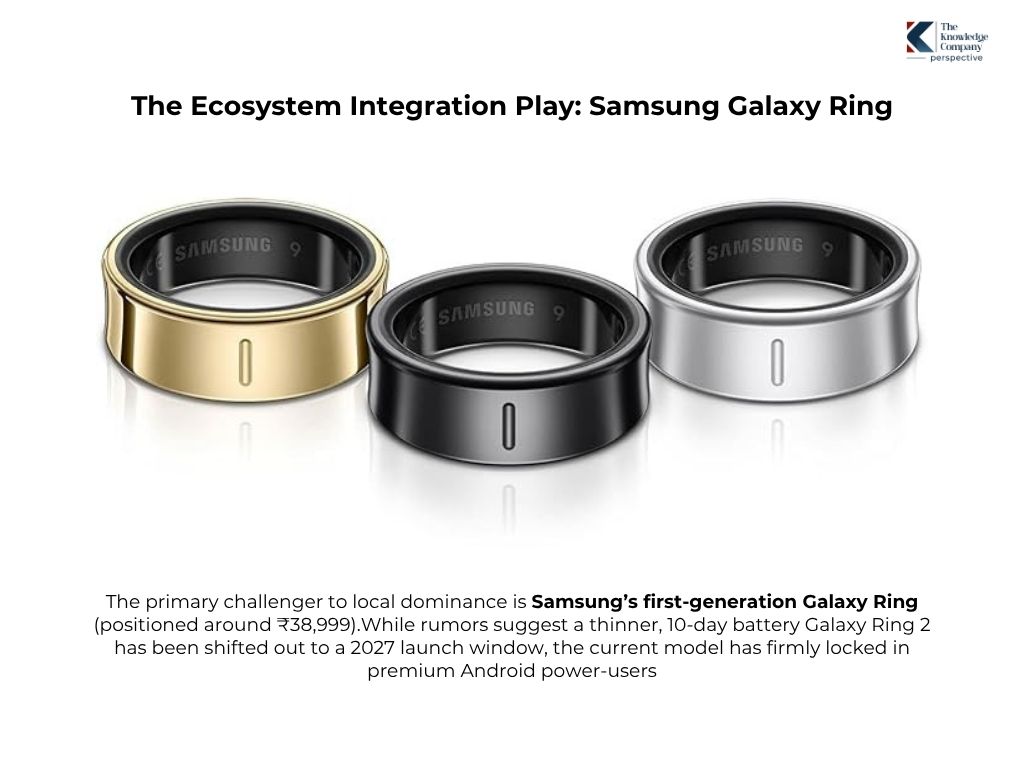

The primary challenger to local dominance is Samsung’s first-generation Galaxy Ring (positioned around ₹38,999).While rumors suggest a thinner, 10-day battery Galaxy Ring 2 has been shifted out to a 2027 launch window, the current model has firmly locked in premium Android power-users.

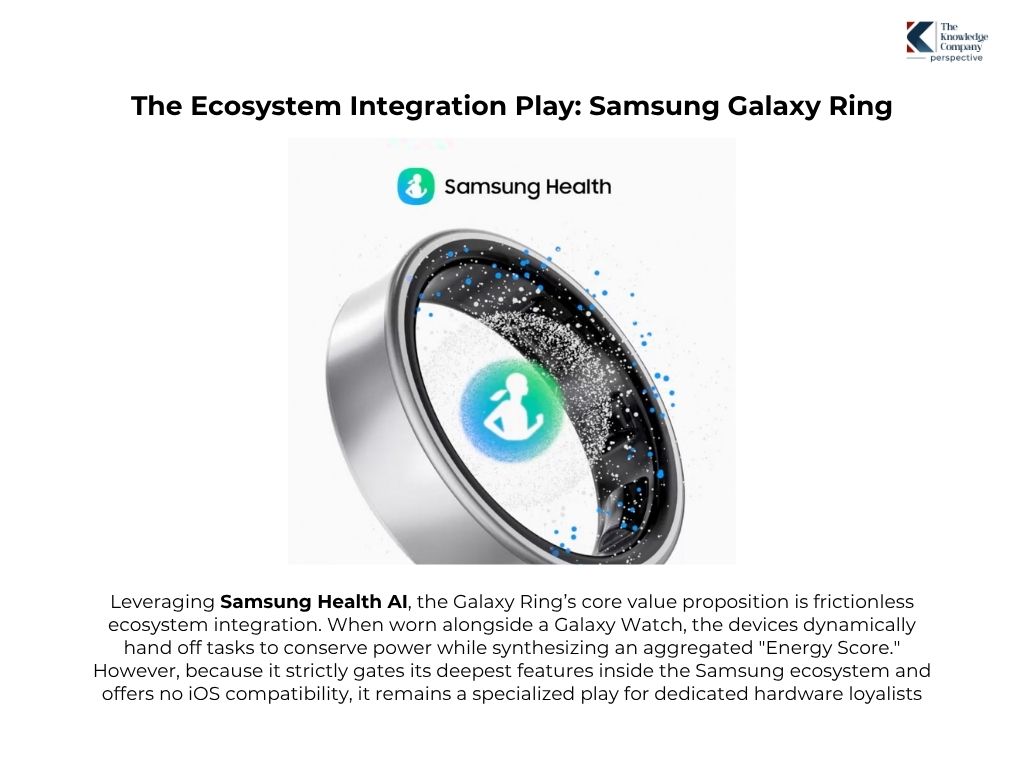

Leveraging Samsung Health AI, the Galaxy Ring’s core value proposition is frictionless ecosystem integration. When worn alongside a Galaxy Watch, the devices dynamically hand off tasks to conserve power while synthesizing an aggregated “Energy Score.” However, because it strictly gates its deepest features inside the Samsung ecosystem and offers no iOS compatibility, it remains a specialized play for dedicated hardware loyalists.

The mid-and-lower market tiers are characterized by aggressive feature-stacking to capture value-conscious consumers.

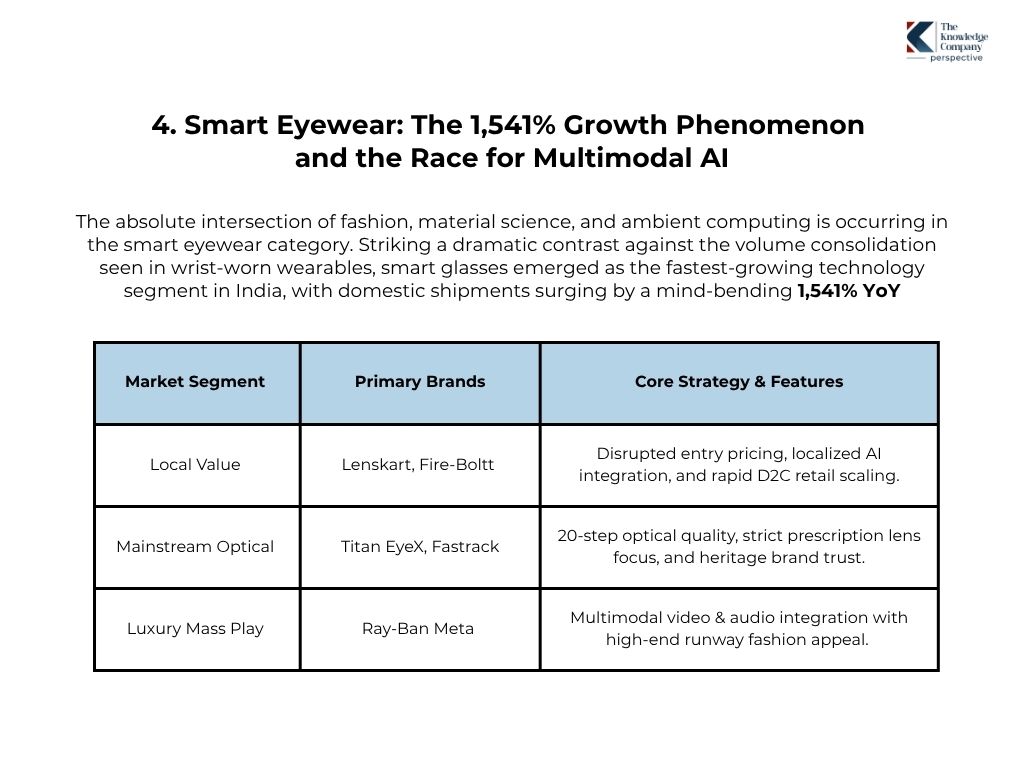

The absolute intersection of fashion, material science, and ambient computing is occurring in the smart eyewear category. Striking a dramatic contrast against the volume consolidation seen in wrist-worn wearables, smart glasses emerged as the fastest-growing technology segment in India, with domestic shipments surging by a mind-bending 1,541% YoY.

This astronomical growth curve highlights a fundamental psychological shift in the Indian consumer base: the acceptance of technology on the face, provided it functions flawlessly as a high-style fashion accessory. The market has moved rapidly past basic “audio sunglasses” to integrated, multimodal AI eyewear that acts as a hands-free portal to the digital world.

The competitive matrix of the Indian smart eyewear landscape is a high-stakes standoff between an aggressive, tech-first D2C ecosystem, legacy optical giants, and luxury global tech.

The Market Disruption: Lenskart’s Aggressive Early Access Play

Omnichannel optical unicorn Lenskart controls the largest slice of the domestic pie with a 36.2% market share.

Lenskart completely disrupted the pricing matrix by rolling out early-access programs for its highly anticipated AI Smart Glasses range. Positioned deliberately below global tech-conglomerate alternatives, Lenskart’s strategic masterstroke has been leveraging its vast, 1,500+ brick-and-mortar retail footprint across India. By treating smart glasses not as a specialized tech gadget, but as an easily customizable frame that can be fitted with blue-cut, power, or transition lenses within an hour at any local outlet, they have dismantled the primary barrier to mass adoption.

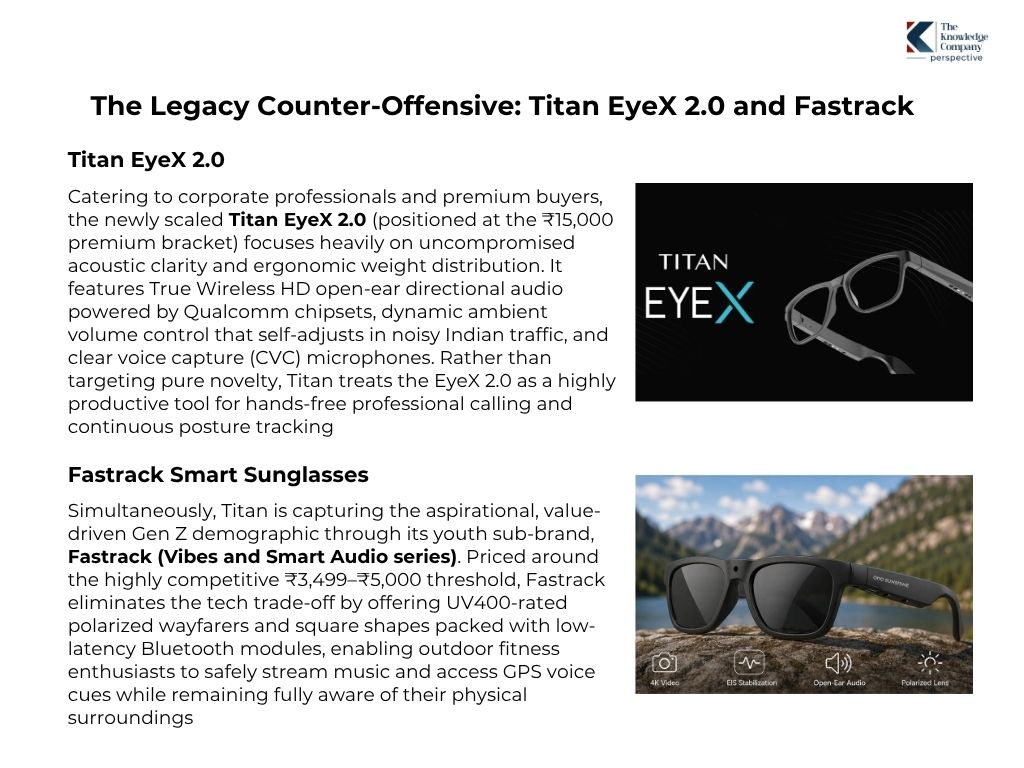

Not to be outdone by agile D2C upstarts, Titan Company Limited has successfully commercialized its electronic eyewear division by relying on decade-long consumer trust and clinical eyecare credentials.

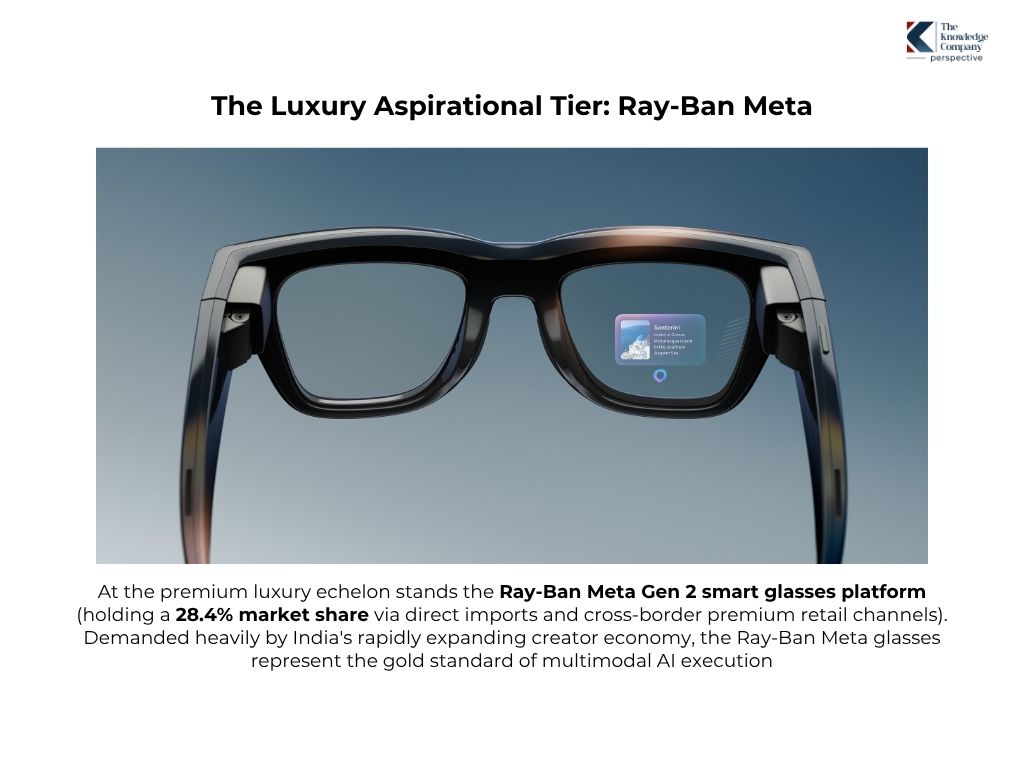

At the premium luxury echelon stands the Ray-Ban Meta Gen 2 smart glasses platform (holding a 28.4% market share via direct imports and cross-border premium retail channels). Demanded heavily by India’s rapidly expanding creator economy, the Ray-Ban Meta glasses represent the gold standard of multimodal AI execution.

Featuring an ultra-discreet 12MP camera, these glasses allow influencers and travel vloggers to livestream directly to Instagram completely hands-free from a first-person perspective. The underlying AI architecture allows users to look at an Indian historical monument or a menu in a foreign language and say, “Hey Meta, look and translate,” processing complex visual-to-text queries in real-time.

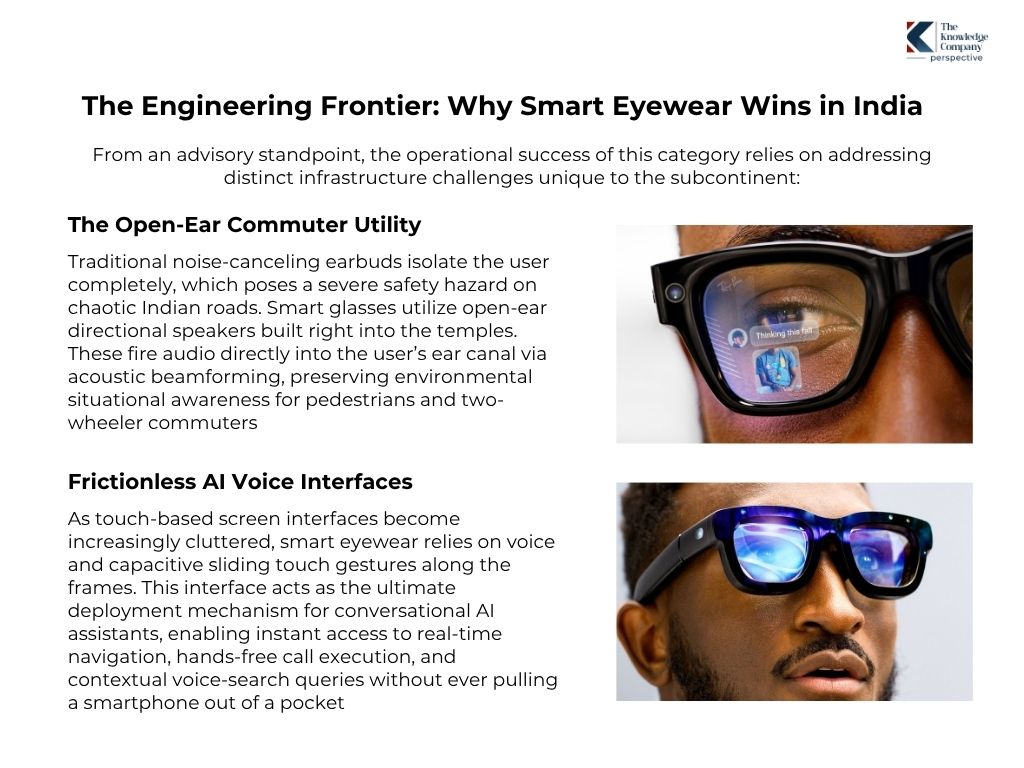

From an advisory standpoint, the operational success of this category relies on addressing distinct infrastructure challenges unique to the subcontinent:

The prevailing design philosophy of 2026 dictates that a garment or accessory should possess advanced technological utility while remaining visually indistinguishable from standard fashion. Moving aggressively past the era of rigid, plastic tracking devices strapped to the body, the Indian apparel sector is experiencing an unprecedented structural convergence with material science—a paradigm shift known as “Wearables 2.0.”

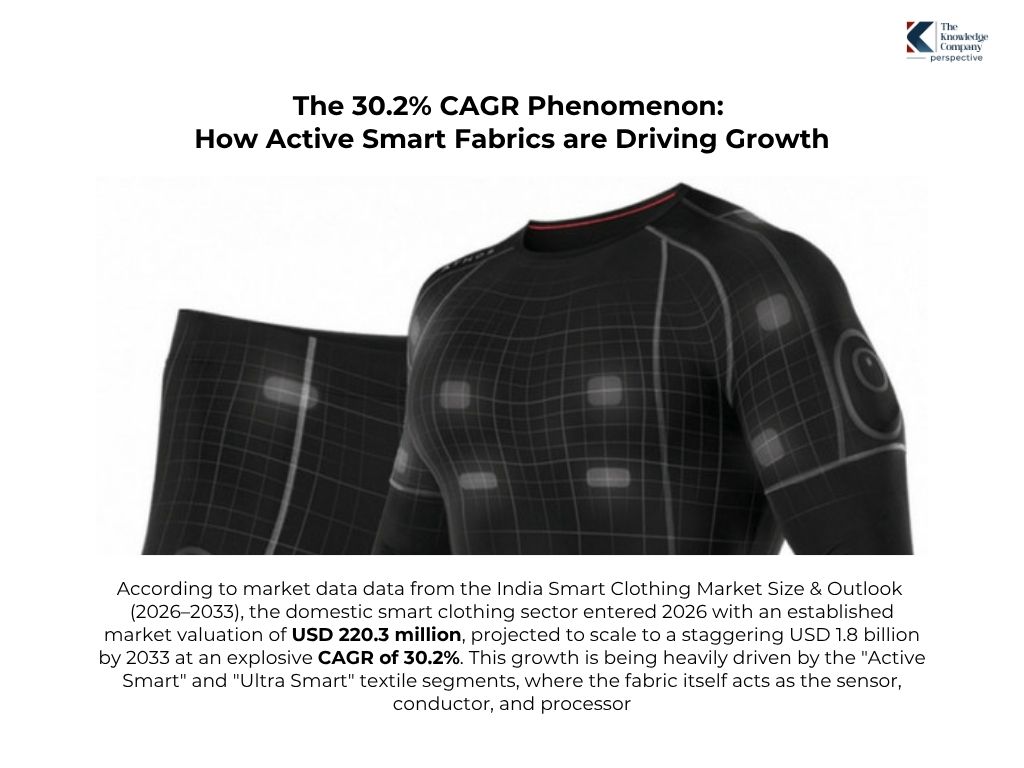

According to market data data from the India Smart Clothing Market Size & Outlook (2026–2033), the domestic smart clothing sector entered 2026 with an established market valuation of USD 220.3 million, projected to scale to a staggering USD 1.8 billion by 2033 at an explosive CAGR of 30.2%. This growth is being heavily driven by the “Active Smart” and “Ultra Smart” textile segments, where the fabric itself acts as the sensor, conductor, and processor.

Given India’s extreme and shifting climatic conditions, functionality is the primary driver of modern apparel choices. The industry is seeing a massive surge in smart ethnic wear designed to combat severe metropolitan heatwaves.

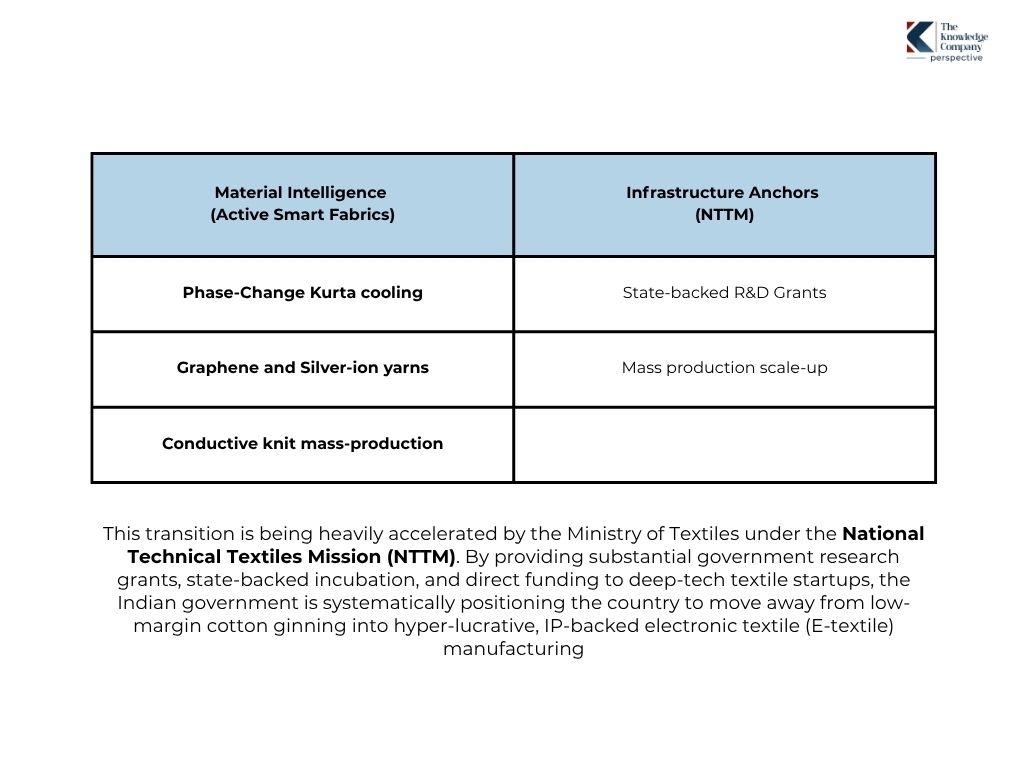

Domestic d2c disruptors and legacy suppliers are engineering self-cooling kurtas and corporate formal shirts using phase-change materials (PCMs) and encapsulated micro-hydrogels directly embedded into organic cotton threads. When ambient temperatures spike past 38°C, these micro-capsules liquefy, absorbing excess body heat and storing it. When the wearer enters an air-conditioned room, the materials solidify again, releasing the stored heat and keeping the microscopic micro-climate of the garment at a consistent, comfortable temperature.

Furthermore, smart-apparel pioneers like Turms have successfully scaled mass-market production of smart denims and tees utilizing silver-ion and nanotechnology that offer 30-day anti-odor properties and liquid-repellent surfaces, drastically dropping water consumption and catering heavily to the lifestyle demands of Gen Z.

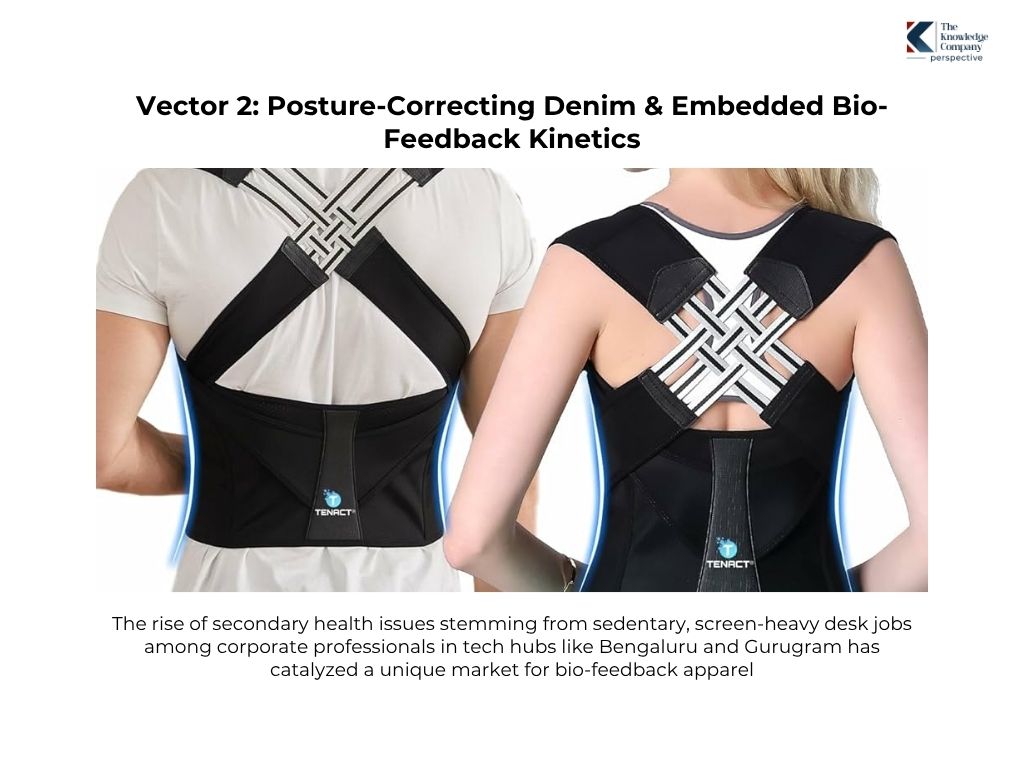

The rise of secondary health issues stemming from sedentary, screen-heavy desk jobs among corporate professionals in tech hubs like Bengaluru and Gurugram has catalyzed a unique market for bio-feedback apparel.

Next-generation slim-fit jeans and structured blazers are now being manufactured with microscopic, hyper-flexible strain gauge sensors integrated completely invisibly within the fabric waistbands and shoulder seams. Homegrown premium labels—such as VeechiVed, which explores the intersection of traditional philosophy and slow, conscious tech-weaving—are analyzing how modern silhouettes can actively assist wellness. These embedded conductive yarns continuously measure localized tension. The moment a user slouches or sustains poor spinal alignment for more than 45 seconds, the garment triggers a silent, localized haptic vibration via an ultra-thin, coin-sized actuator embedded in the rear lining, delivering a physical nudge to correct posture.

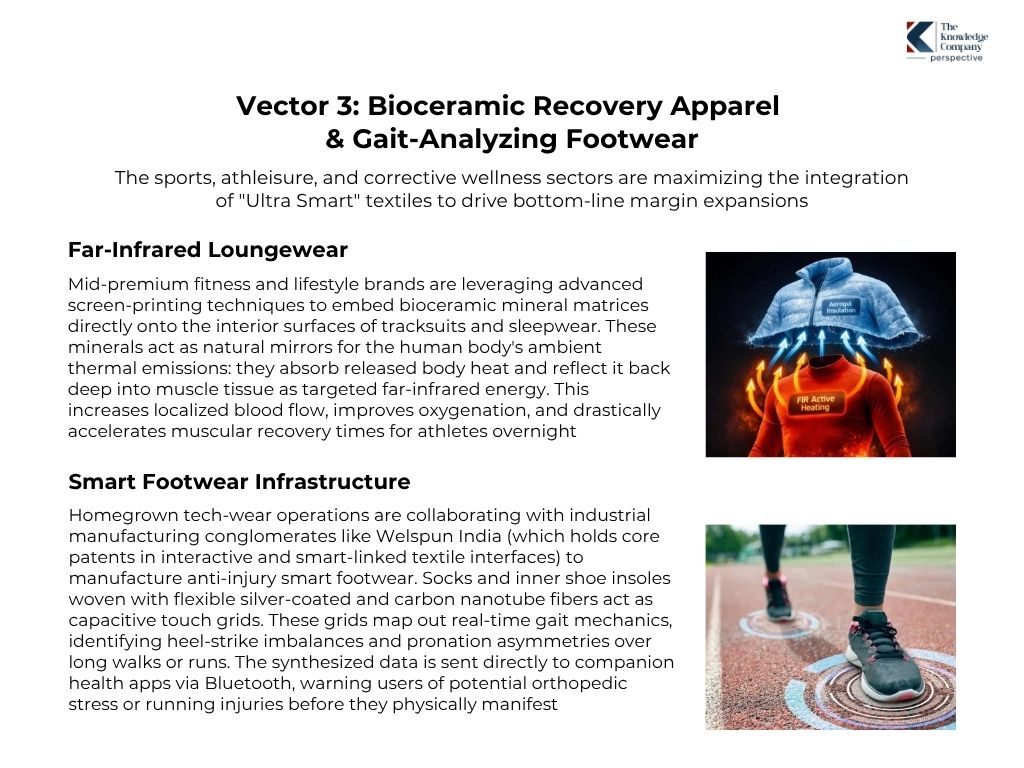

The sports, athleisure, and corrective wellness sectors are maximizing the integration of “Ultra Smart” textiles to drive bottom-line margin expansions.

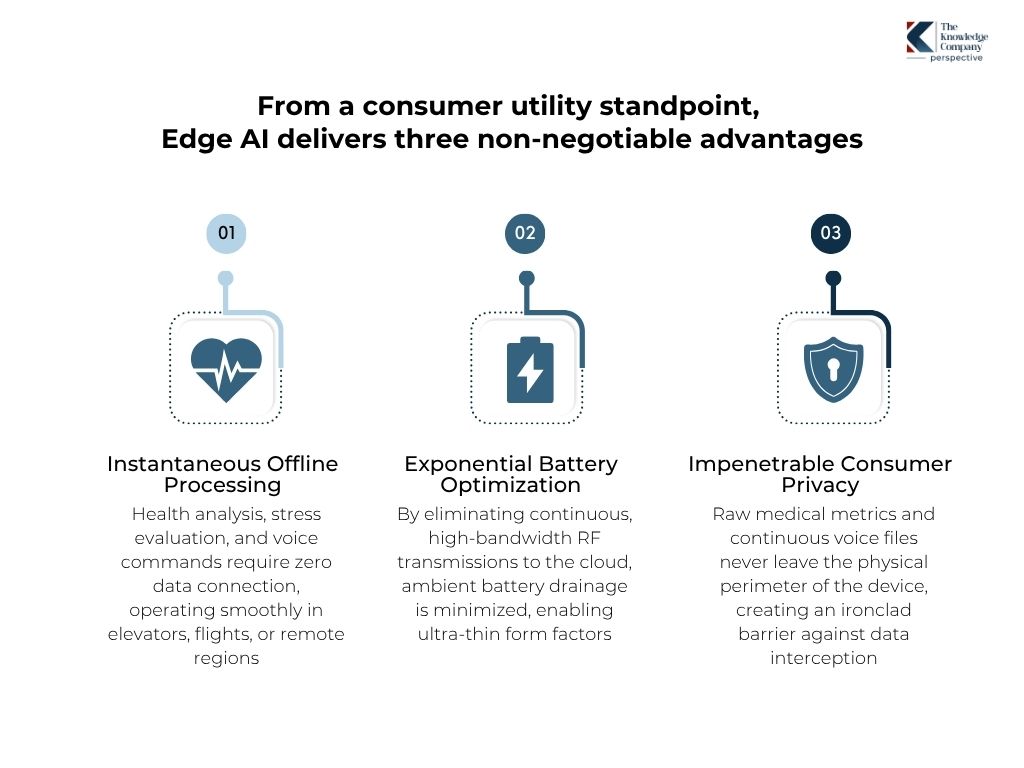

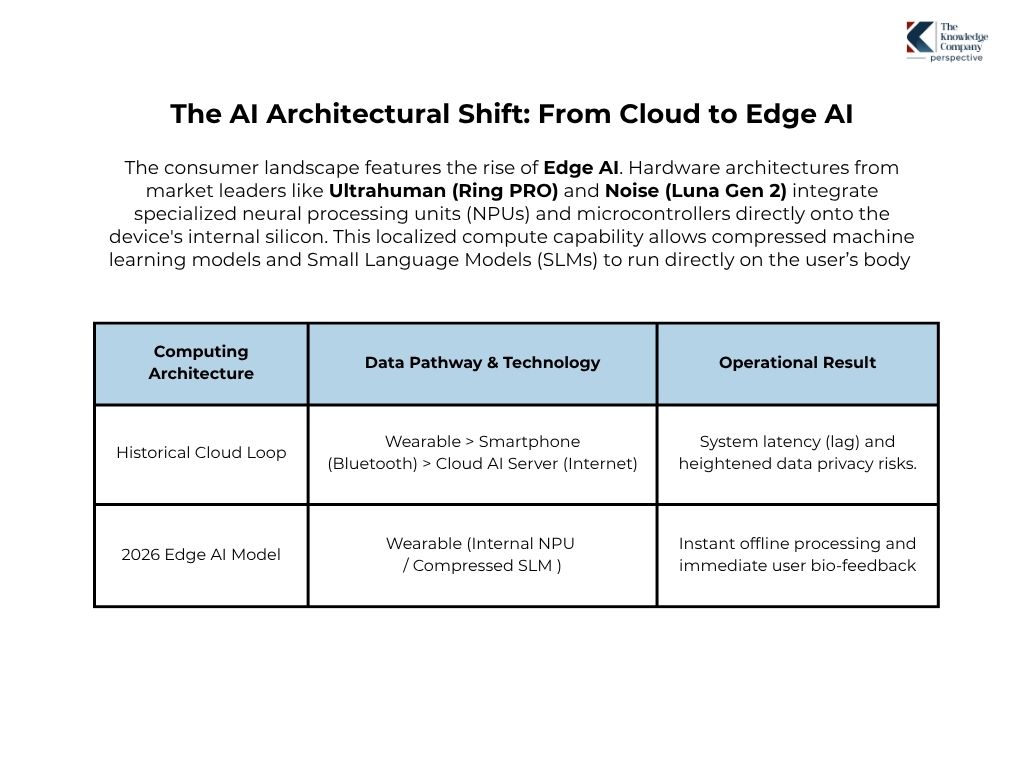

The absolute pivot point defining the Indian wearable ecosystem is a profound architectural migration in processing location and intelligence deployment. The era of treating a wearable device as a passive, “dumb” data harvester that merely pumps raw metrics back to a cloud server is over.

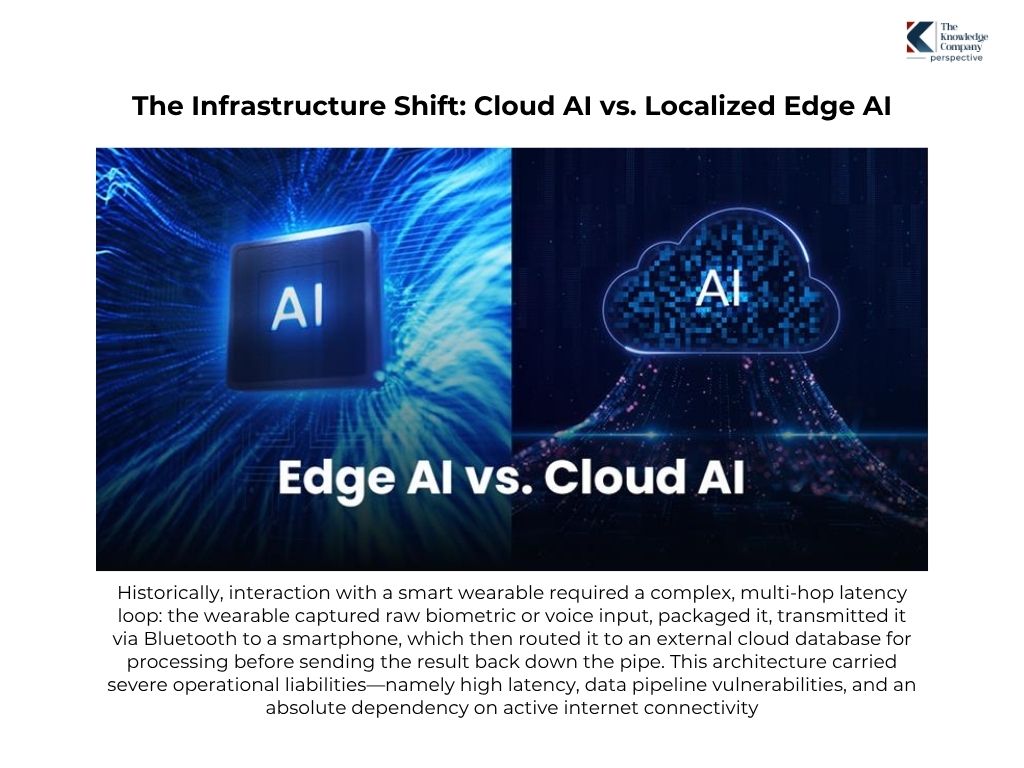

Historically, interaction with a smart wearable required a complex, multi-hop latency loop: the wearable captured raw biometric or voice input, packaged it, transmitted it via Bluetooth to a smartphone, which then routed it to an external cloud database for processing before sending the result back down the pipe. This architecture carried severe operational liabilities—namely high latency, data pipeline vulnerabilities, and an absolute dependency on active internet connectivity.

The consumer landscape features the rise of Edge AI. Hardware architectures from market leaders like Ultrahuman (Ring PRO) and Noise (Luna Gen 2) integrate specialized neural processing units (NPUs) and microcontrollers directly onto the device’s internal silicon. This localized compute capability allows compressed machine learning models and Small Language Models (SLMs) to run directly on the user’s body.

From a consumer utility standpoint, Edge AI delivers three non-negotiable advantages:

To unlock exponential growth avenues beyond saturated Tier-1 metros and capture the emerging consumer base in Tier-2 and Tier-3 geographies, wearable brands have systematically localized their AI interfaces.

Generic, Western-centric voice recognition software is inherently incompatible with the linguistic diversity of the Indian market. Homegrown players have engineered conversational AI layers capable of natively processing localized dialects on the edge.

By deploying speech-recognition models fine-tuned to accept multi-lingual queries and localized speech patterns, the interface barrier has been completely democratized. A user can interact with their hardware in Hindi, Tamil, Telugu, Kannada, or Bengali—commanding a device to evaluate sleep scores, trace historical heart rate patterns, or parse real-time environmental metrics via vocal prompts without ever touching a digital screen.

India’s aggressive ambition to transition from a secondary technology assembler into an unassailable global innovation hub is heavily reinforced by state policy. This dual framework of stringent legal compliance and historic manufacturing subsidies is entirely reshaping the risk-and-reward calculus for consumer electronics brands.

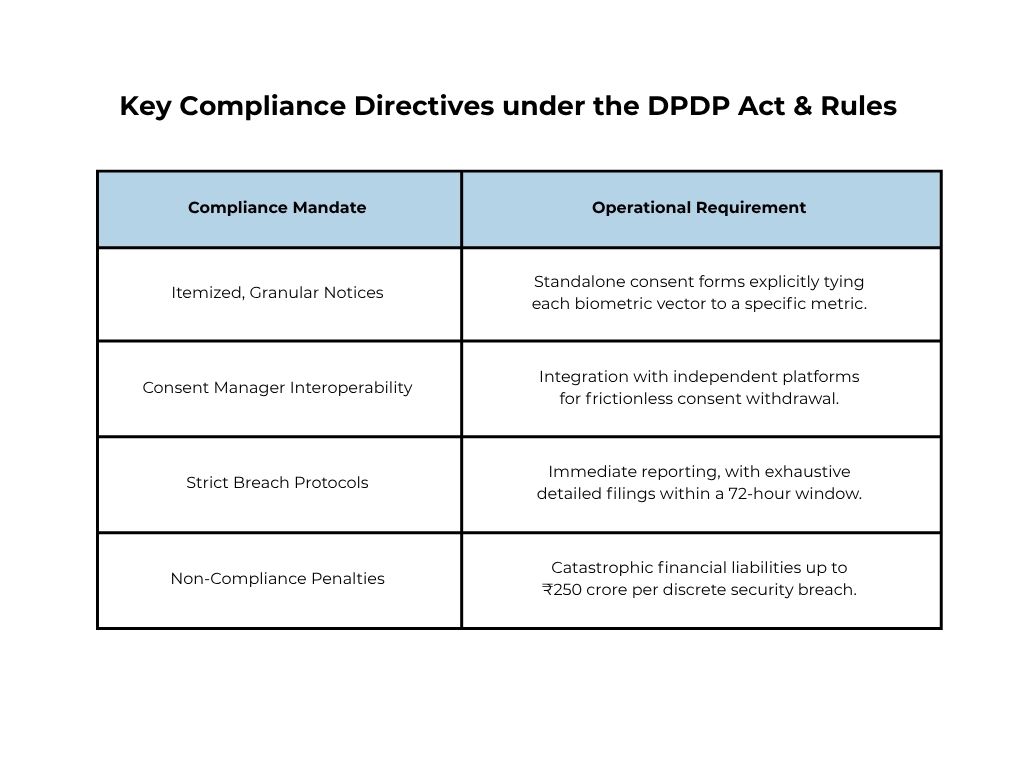

With the formal notification and operationalization of the Digital Personal Data Protection (DPDP) Rules, the legal landscape for tech-wear operations has dramatically transformed.

Because modern smart rings, continuous biometric sensors, and AI hearables ingest real-time physiological data, wearable companies are legally classified as Data Fiduciaries dealing with high-risk personal data. Under this strict framework, the old practices of passive, hidden, pre-checked data agreements are illegal.

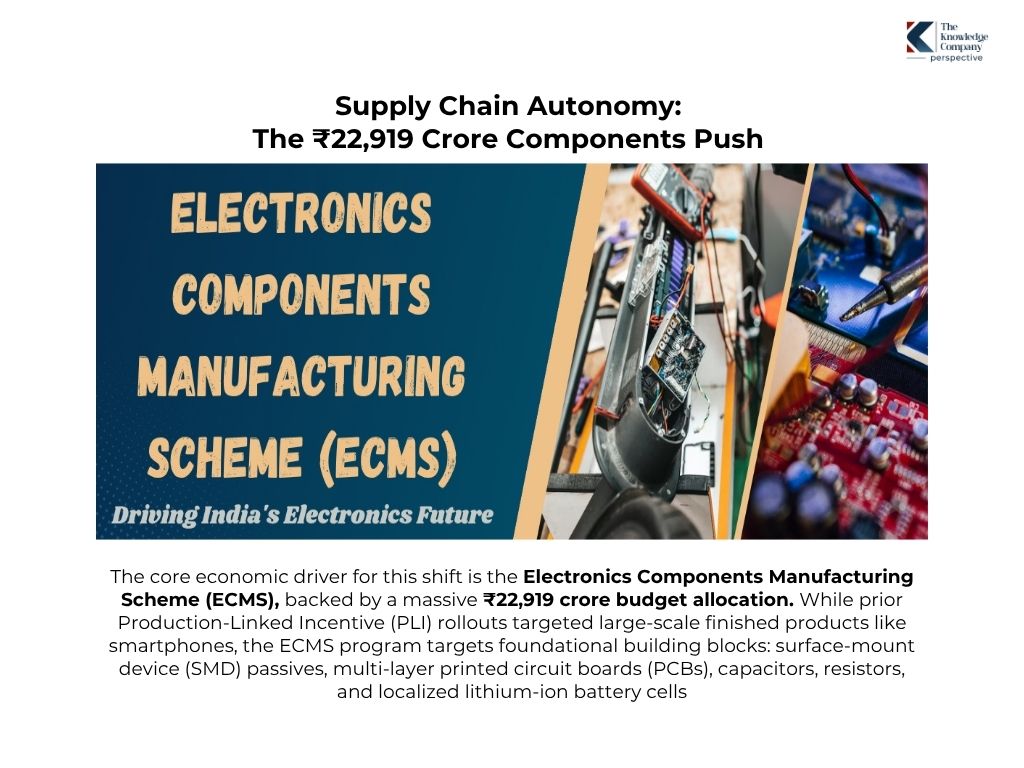

On the infrastructure front, the Indian government has moved decisively past the basic assembly of completely knocked-down (CKD) kits to foster a deep, component-level manufacturing ecosystem.

The core economic driver for this shift is the Electronics Components Manufacturing Scheme (ECMS), backed by a massive ₹22,919 crore budget allocation. While prior Production-Linked Incentive (PLI) rollouts targeted large-scale finished products like smartphones, the ECMS program targets foundational building blocks: surface-mount device (SMD) passives, multi-layer printed circuit boards (PCBs), capacitors, resistors, and localized lithium-ion battery cells.

According to official Invest India and PIB updates, expected investment commitments under this component drive have crossed ₹1.15 lakh crore, with dozens of high-tech production plants successfully cleared across multiple states.

By heavily subsidizing local capital expenditure and linking direct payouts to stringent quality standards, the government is enabling domestic giants like boAt (Imagine Marketing) and Noise to systematically swap out imported components sourced from China or Taiwan. This deep domestic value addition (DVA) significantly lowers bill-of-materials (BOM) costs, de-risks local assembly from global supply chain shocks, and provides the exact economic leverage needed for Indian brands to scale aggressively into international export markets across Southeast Asia and the Middle East.

The Indian wearable technology market in 2026 is definitively characterized by the rapid, forced transformation of both the consumer and the technology itself. The profound convergence of high fashion and ambient technology indicates that the future of the industry lies not in screens, but in invisible, ambient intelligence.

At TKC, our advisory practice recognizes that the victors in this revolution will be those entities capable of orchestrating a highly complex matrix.

Brands must deliver medically validated, Edge AI-driven insights wrapped in culturally resonant fashion, financed through frictionless embedded credit, and anchored by unassailable data privacy architectures.

Reach out to our expert team at TKC to build a resilient, future-proof strategy for the next era of connected wearables.