")

Introduction: The Transformation of the Indian Apparel Ecosystem

The Indian fashion and apparel landscape is undergoing a structural and cultural metamorphosis of unprecedented scale. Moving aggressively away from a highly fragmented, unorganized local marketplace, India has cemented its status as a globally integrated retail powerhouse. As legacy retail markets in the United States, Europe, Japan, and China experience plateauing growth around or below the 5% mark, India has emerged as the global retail sector’s most critical and reliable growth engine.

This upward trajectory is not merely a function of population growth; it is the direct result of a profound formalization of the retail sector. Historically dominated by unorganized local “mom-and-pop” markets, the share of organized retail has captured an estimated 45% of the apparel market. By 2030, digital online platforms, exclusive brand outlets (EBOs), and organized multi-brand retail chains are anticipated to account for over 60% of all apparel purchases nationwide. For global brands like Inditex (Zara), H&M, and Fast Retailing (Uniqlo), India functions as a live, high-stakes testbed for growth, relevance, and reinvention.

The Demographic Paradigm Shift: From Gen Z to the “Silver Tsunami”

The traditional archetypes of the Indian apparel consumer have fractured into highly distinct, value-driven cohorts. With India projected to become the third-largest consumer market globally, brands can no longer rely on monolithic marketing strategies; they must navigate a complex matrix of generational demands.

Generation Z and the Circular Fashion Economy

At the epicenter of the urban casualwear revolution is India’s Generation Z, a massive demographic cohort numbering 377 million and representing roughly 40% of the nation’s population. Modern Indian youth are systematically dismantling the linear consumption model. They demand stringent sustainability, brand authenticity, and cultural resonance.

This ideological shift has catalyzed the explosive growth of the recommerce and circular fashion sectors. The Indian recommerce market—driven by digital-first platforms like FreeUp, Relove, and countless hyper-active Instagram thrift ecosystems—is scaling toward a multi-billion-dollar valuation with double-digit annual growth. Mainstream retailers are actively establishing dedicated thrift and resale partnerships. They recognize that secondary lifecycles of garments not only improve the return on investment for sustainability initiatives but also lower long-term sourcing costs by reintroducing high-quality materials into the circular supply chain.

The Rise of the Silver Economy and Adaptive Casualwear

Simultaneously, India is experiencing a profound demographic aging process. By 2036, the senior citizen population is projected to surge to approximately 230 million, making up about 15% of the total population. This “Silver Tsunami” represents a massive, largely untapped reservoir of discretionary spending. The organized senior care industry has surged past its baseline $10–$15 billion valuation, eyeing an expansion toward $30–$50 billion over the next decade.

Older consumers are exhibiting a marked departure from traditional, rigid ethnic wear, increasingly favoring “Affordable Fashionable Comfort.” A critical sub-sector emerging here is adaptive clothing. With roughly 3% of the Indian population living with some form of disability and advancing age bringing inevitable declines in mobility, adaptive casualwear is transitioning from niche to essential.

Pioneering domestic brands like Haxor and Anucool are engineering everyday garments with magnetic closures, VELCRO® brand fasteners, open-back features, and easy-touch elastic waists. These designs provide dignity and independence to the elderly while easing the burden on caregivers. They successfully merge vital medical utility with modern casualwear aesthetics, creating a highly lucrative and socially responsible market segment.

Retail Reinvention: The Quick Commerce Disruption in Apparel

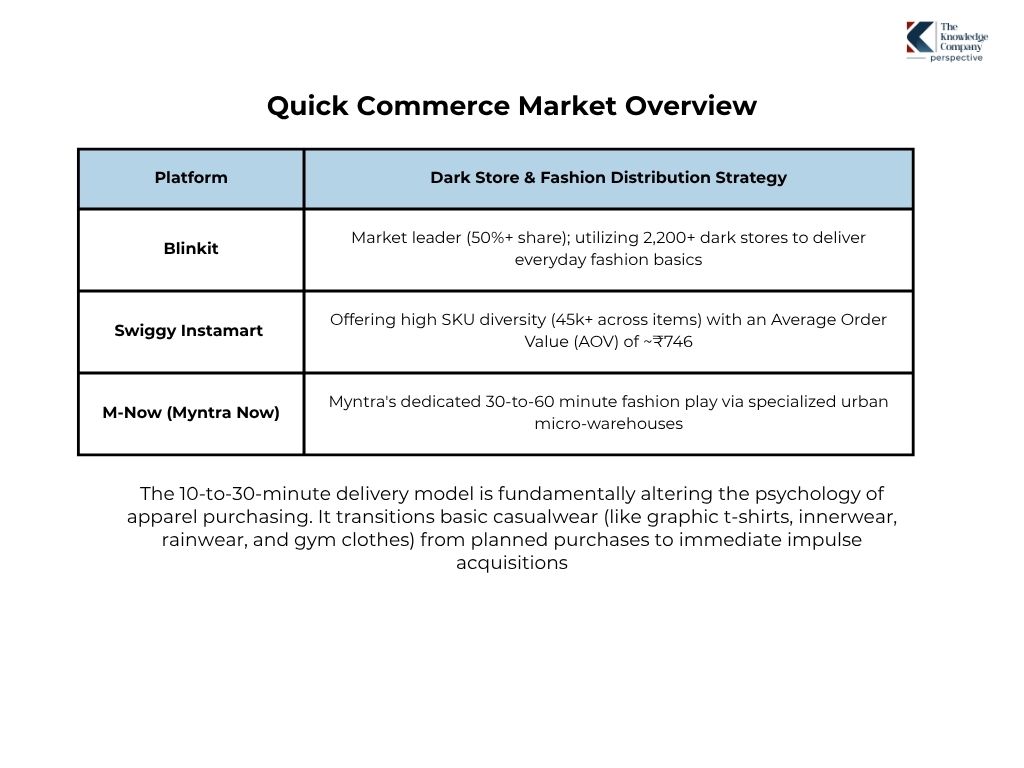

The architecture of retail distribution in India is undergoing a severe compression. The traditional consumer journey—which historically spanned days of browsing, trying, and buying—has been reduced to a matter of minutes by the aggressive expansion of quick commerce (q-commerce) platforms into the fashion and casualwear segments.

The Indian quick commerce market—dominated by heavyweights Blinkit, Swiggy Instamart, Zepto, and the newly scaled Flipkart Minutes—saw its gross order value (GOV) cross an estimated ₹64,000 crore (~$7.6 billion) in FY25, growing at over 100% year-on-year. While initially reliant on low-margin groceries, these platforms are aggressively leveraging high-margin non-grocery categories, particularly apparel, electronics, and lifestyle accessories, to achieve EBITDA break-even and drive margin expansion.

The 10-to-30-minute delivery model is fundamentally altering the psychology of apparel purchasing. It transitions basic casualwear (like graphic t-shirts, innerwear, rainwear, and gym clothes) from planned purchases to immediate impulse acquisitions.

Logistical Note on the Q-Commerce Shift

Managing apparel in dark stores presents unique logistical challenges compared to groceries. To combat the complexities of exact sizing, platforms focus heavily on “forgiving” silhouettes—free-size garments, basic S/M/L t-shirts, innerwear, socks, and jewelry—minimizing the risk of high return rates while maximizing dark store shelf efficiency.

Design and Localization: Climate, Culture, and the “Un-Ethnic” Aesthetic

The success of casualwear and urbanwear in India is intrinsically linked to how well brands can localize global trends to suit the subcontinent’s diverse climates and rich cultural heritage. The modern Indian consumer actively rejects the blind adoption of Western silhouettes if they compromise functional comfort.

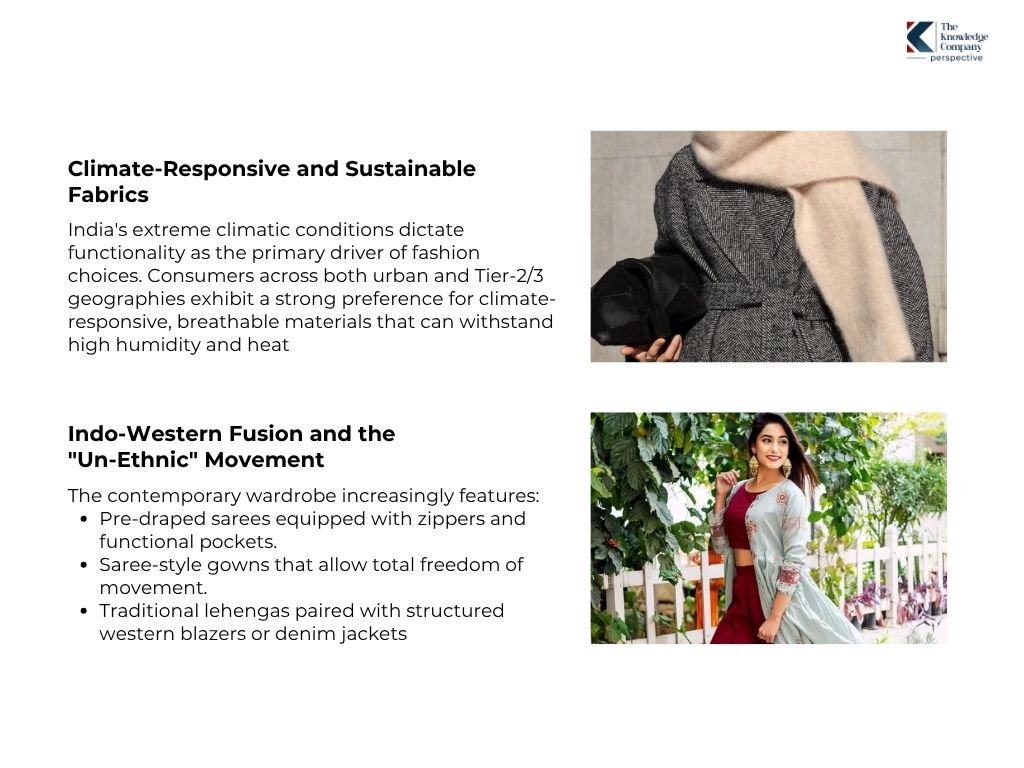

Saree-style gowns that allow total freedom of movement.

Traditional lehengas paired with structured western blazers or denim jackets.

Conclusion: Weaving a Modern Future

The Great Indian Wardrobe Reformation is well underway. The ethnicwear market is at a pivotal moment, transitioning from a fragmented, craft-based past to a structured, corporate-led future.

The sleepy, predictable rhythm of festive seasons is being replaced by the dynamic, year-round hum of a modern apparel industry.

The challenges are significant, rooted in the deep complexities of the supply chain and the volatility of the economic environment.

However, the opportunities are even greater. The consumer is sending clear signals: they want brands that respect tradition but embrace modernity; that offer beautiful design but also stand for quality and transparency; that are accessible online but also tangible in a physical space.

The future leaders of the Indian ethnicwear market will be the entities that can master this duality—building aspirational, consumer-centric brands on the front end, while simultaneously engineering a resilient, efficient, and technology-enabled supply chain on the back end.

The process will be complex, but for those who can successfully weave together these threads of tradition and transformation, the prize will be a dominant share in one of the world’s most exciting consumer growth stories.

The Indian

fashion and apparel landscape is undergoing a structural and cultural

metamorphosis of unprecedented scale. Moving aggressively away from a highly

fragmented, unorganized local marketplace, India has cemented its status as a

globally integrated retail powerhouse. As legacy retail markets in the United

States, Europe, Japan, and China experience plateauing growth around or below

the 5% mark, India has emerged as the global retail sector’s most critical and

reliable growth engine.

This upward

trajectory is not merely a function of population growth; it is the direct

result of a profound formalization of the retail sector. Historically dominated

by unorganized local “mom-and-pop” markets, the share of organized

retail has captured an estimated 45% of the apparel market. By 2030, digital

online platforms, exclusive brand outlets (EBOs), and organized multi-brand

retail chains are anticipated to account for over 60% of all apparel purchases

nationwide. For global brands like Inditex (Zara), H&M, and Fast Retailing

(Uniqlo), India functions as a live, high-stakes testbed for growth, relevance,

and reinvention.

The Demographic Paradigm Shift: From Gen Z to the “Silver Tsunami”

The traditional archetypes of the Indian apparel consumer have fractured into highly distinct, value-driven cohorts. With India projected to become the third-largest consumer market globally, brands can no longer rely on monolithic marketing strategies; they must navigate a complex matrix of generational demands.

Generation Z and the Circular Fashion Economy

At the epicenter of the urban casualwear revolution is India’s Generation Z, a massive demographic cohort numbering 377 million and representing roughly 40% of the nation’s population. Modern Indian youth are systematically dismantling the linear consumption model. They demand stringent sustainability, brand authenticity, and cultural resonance.

This ideological shift has catalyzed the explosive growth of the recommerce and circular fashion sectors. The Indian recommerce market—driven by digital-first platforms like FreeUp, Relove, and countless hyper-active Instagram thrift ecosystems—is scaling toward a multi-billion-dollar valuation with double-digit annual growth. Mainstream retailers are actively establishing dedicated thrift and resale partnerships. They recognize that secondary lifecycles of garments not only improve the return on investment for sustainability initiatives but also lower long-term sourcing costs by reintroducing high-quality materials into the circular supply chain.

The Rise of the Silver Economy and Adaptive Casualwear

Simultaneously, India is experiencing a profound demographic aging process. By 2036, the senior citizen population is projected to surge to approximately 230 million, making up about 15% of the total population. This “Silver Tsunami” represents a massive, largely untapped reservoir of discretionary spending. The organized senior care industry has surged past its baseline $10–$15 billion valuation, eyeing an expansion toward $30–$50 billion over the next decade.

Older consumers are exhibiting a marked departure from traditional, rigid ethnic wear, increasingly favoring “Affordable Fashionable Comfort.” A critical sub-sector emerging here is adaptive clothing. With roughly 3% of the Indian population living with some form of disability and advancing age bringing inevitable declines in mobility, adaptive casualwear is transitioning from niche to essential.

Pioneering domestic brands like Haxor and Anucool are engineering everyday garments with magnetic closures, VELCRO® brand fasteners, open-back features, and easy-touch elastic waists. These designs provide dignity and independence to the elderly while easing the burden on caregivers. They successfully merge vital medical utility with modern casualwear aesthetics, creating a highly lucrative and socially responsible market segment.

Retail Reinvention: The Quick Commerce Disruption in Apparel

The architecture of retail distribution in India is undergoing a severe compression. The traditional consumer journey—which historically spanned days of browsing, trying, and buying—has been reduced to a matter of minutes by the aggressive expansion of quick commerce (q-commerce) platforms into the fashion and casualwear segments.

The Indian quick commerce market—dominated by heavyweights Blinkit, Swiggy Instamart, Zepto, and the newly scaled Flipkart Minutes—saw its gross order value (GOV) cross an estimated ₹64,000 crore (~$7.6 billion) in FY25, growing at over 100% year-on-year. While initially reliant on low-margin groceries, these platforms are aggressively leveraging high-margin non-grocery categories, particularly apparel, electronics, and lifestyle accessories, to achieve EBITDA break-even and drive margin expansion.

|

|

Organised Brands |

Unorganised Sector |

Industry Average |

|

Platform |

48% |

32% |

41% |

|

Blinkit |

18% |

9% |

14% |

|

Swiggy Instamart |

3.1x |

2.2x |

2.6x |

These benchmarks highlight the significant operational advantages of the organised players.

Their higher gross margins are a result of better sourcing power and brand-based pricing, while superior EBITDA margins reflect greater operational leverage.

The higher inventory turnover rate (3.1x vs. 2.2x) is particularly critical, indicating a more efficient conversion of inventory into sales, which minimizes working capital requirements and reduces the risk of seasonal markdowns—a key challenge in this trend-driven industry.

The Competitive Landscape: The Era of Corporate Consolidation

The single most significant trend shaping the industry today is the entry and expansion of large, well-capitalized corporate entities.

These players are leveraging their financial muscle, retail expertise, and supply chain networks to consolidate the fragmented market, primarily through strategic acquisitions and the launch of new, scalable brands.

The competitive landscape is now composed of several distinct tiers:

Brands such as Libas, House of Chikankari, and The Loom have used social commerce, influencer marketing, and quick trend cycles to scale rapidly.

The growth rate for D2C brands in the ethnicwear category has consistently outpaced that of the broader apparel market, demonstrating the power of a digital-first approach.

Despite the positive demand environment, the ethnicwear industry is fraught with deep-seated structural challenges and is susceptible to macro-economic volatility. These headwinds can significantly impact profitability and scalability.

The most significant challenge lies in supply chain fragmentation. Unlike the fast-fashion industry, which relies on large, consolidated manufacturing units, a significant portion of ethnicwear production is dependent on a scattered network of small-scale artisans, weavers, and printing units.

This creates immense complexity in ensuring quality control, production consistency, and on-time delivery at scale. The high degree of manual dependency makes the supply chain less agile and more vulnerable to disruptions.

This complexity feeds directly into the challenge of inventory and SKU management. The ethnicwear market is characterized by immense regional taste variations, high seasonality tied to a diverse calendar of festivals, and fast-changing design trends.

A design that is a bestseller in North India for Diwali may have no takers in the South during Pongal. This requires brands to manage a vast and complex array of SKUs (Stock Keeping Units), leading to a high risk of inventory obsolescence and the need for deep seasonal discounting, which erodes gross margins.

Furthermore, the industry is exposed to macro and geopolitical factors:

For brands and investors seeking to navigate this evolving landscape, success will be determined by the ability to address the industry’s structural challenges while capitalizing on the new consumer trends. Several strategic imperatives are clear:

The Great Indian Wardrobe Reformation is well underway. The ethnicwear market is at a pivotal moment, transitioning from a fragmented, craft-based past to a structured, corporate-led future.

The sleepy, predictable rhythm of festive seasons is being replaced by the dynamic, year-round hum of a modern apparel industry.

The challenges are significant, rooted in the deep complexities of the supply chain and the volatility of the economic environment.

However, the opportunities are even greater. The consumer is sending clear signals: they want brands that respect tradition but embrace modernity; that offer beautiful design but also stand for quality and transparency; that are accessible online but also tangible in a physical space.

The future leaders of the Indian ethnicwear market will be the entities that can master this duality—building aspirational, consumer-centric brands on the front end, while simultaneously engineering a resilient, efficient, and technology-enabled supply chain on the back end.

The process will be complex, but for those who can successfully weave together these threads of tradition and transformation, the prize will be a dominant share in one of the world’s most exciting consumer growth stories.

The Indian fashion and apparel landscape is undergoing a structural and cultural metamorphosis of unprecedented scale. Moving aggressively away from a highly fragmented, unorganized local marketplace, India has cemented its status as a globally integrated retail powerhouse. As legacy retail markets in the United States, Europe, Japan, and China experience plateauing growth around or below the 5% mark, India has emerged as the global retail sector’s most critical and reliable growth engine.

This upward trajectory is not merely a function of population growth; it is the direct result of a profound formalization of the retail sector. Historically dominated by unorganized local “mom-and-pop” markets, the share of organized retail has captured an estimated 45% of the apparel market. By 2030, digital online platforms, exclusive brand outlets (EBOs), and organized multi-brand retail chains are anticipated to account for over 60% of all apparel purchases nationwide. For global brands like Inditex (Zara), H&M, and Fast Retailing (Uniqlo), India functions as a live, high-stakes testbed for growth, relevance, and reinvention.

The Demographic Paradigm Shift: From Gen Z to the “Silver Tsunami”

The traditional archetypes of the Indian apparel consumer have fractured into highly distinct, value-driven cohorts. With India projected to become the third-largest consumer market globally, brands can no longer rely on monolithic marketing strategies; they must navigate a complex matrix of generational demands.

Generation Z and the Circular Fashion Economy

At the epicenter of the urban casualwear revolution is India’s Generation Z, a massive demographic cohort numbering 377 million and representing roughly 40% of the nation’s population. Modern Indian youth are systematically dismantling the linear consumption model. They demand stringent sustainability, brand authenticity, and cultural resonance.

This ideological shift has catalyzed the explosive growth of the recommerce and circular fashion sectors. The Indian recommerce market—driven by digital-first platforms like FreeUp, Relove, and countless hyper-active Instagram thrift ecosystems—is scaling toward a multi-billion-dollar valuation with double-digit annual growth. Mainstream retailers are actively establishing dedicated thrift and resale partnerships. They recognize that secondary lifecycles of garments not only improve the return on investment for sustainability initiatives but also lower long-term sourcing costs by reintroducing high-quality materials into the circular supply chain.

The Rise of the Silver Economy and Adaptive Casualwear

Simultaneously, India is experiencing a profound demographic aging process. By 2036, the senior citizen population is projected to surge to approximately 230 million, making up about 15% of the total population. This “Silver Tsunami” represents a massive, largely untapped reservoir of discretionary spending. The organized senior care industry has surged past its baseline $10–$15 billion valuation, eyeing an expansion toward $30–$50 billion over the next decade.

Older consumers are exhibiting a marked departure from traditional, rigid ethnic wear, increasingly favoring “Affordable Fashionable Comfort.” A critical sub-sector emerging here is adaptive clothing. With roughly 3% of the Indian population living with some form of disability and advancing age bringing inevitable declines in mobility, adaptive casualwear is transitioning from niche to essential.

Pioneering domestic brands like Haxor and Anucool are engineering everyday garments with magnetic closures, VELCRO® brand fasteners, open-back features, and easy-touch elastic waists. These designs provide dignity and independence to the elderly while easing the burden on caregivers. They successfully merge vital medical utility with modern casualwear aesthetics, creating a highly lucrative and socially responsible market segment.

Retail Reinvention: The Quick Commerce Disruption in Apparel

The architecture of retail distribution in India is undergoing a severe compression. The traditional consumer journey—which historically spanned days of browsing, trying, and buying—has been reduced to a matter of minutes by the aggressive expansion of quick commerce (q-commerce) platforms into the fashion and casualwear segments.

The Indian quick commerce market—dominated by heavyweights Blinkit, Swiggy Instamart, Zepto, and the newly scaled Flipkart Minutes—saw its gross order value (GOV) cross an estimated ₹64,000 crore (~$7.6 billion) in FY25, growing at over 100% year-on-year. While initially reliant on low-margin groceries, these platforms are aggressively leveraging high-margin non-grocery categories, particularly apparel, electronics, and lifestyle accessories, to achieve EBITDA break-even and drive margin expansion.

The 10-to-30-minute delivery model is fundamentally altering the psychology of apparel purchasing. It transitions basic casualwear (like graphic t-shirts, innerwear, rainwear, and gym clothes) from planned purchases to immediate impulse acquisitions.

Logistical Note on the Q-Commerce Shift

Managing apparel in dark stores presents unique logistical challenges compared to groceries. To combat the complexities of exact sizing, platforms focus heavily on “forgiving” silhouettes—free-size garments, basic S/M/L t-shirts, innerwear, socks, and jewelry—minimizing the risk of high return rates while maximizing dark store shelf efficiency.

The success of casualwear and urbanwear in India is intrinsically linked to how well brands can localize global trends to suit the subcontinent’s diverse climates and rich cultural heritage. The modern Indian consumer actively rejects the blind adoption of Western silhouettes if they compromise functional comfort.

India’s extreme climatic conditions dictate functionality as the primary driver of fashion choices. Consumers across both urban and Tier-2/3 geographies exhibit a strong preference for climate-responsive, breathable materials that can withstand high humidity and heat.

The industry is witnessing a surge in the use of next-generation textiles. Khadi Jute, Banana Silk (derived from agricultural waste), regenerated cellulose fabrics like lyocell, and bio-based leather alternatives are dominating contemporary design boards. These materials offer the luxurious finish required by premium urbanwear without the severe ecological footprint of traditional animal agriculture or synthetic plastics.

The strict demarcation between traditional ceremonial ethnic wear and Western casualwear is dissolving, giving rise to the “Un-Ethnic” movement. This involves the complete deconstruction and reimagining of traditional silhouettes into highly functional, globally appealing garments.

The contemporary wardrobe increasingly features:

Fast-fashion brands excel at this, remixing global London or Hollywood trends with breathable local fabrics and a distinct, modern “Bollywood twist.”

Despite explosive top-line growth, retail operators are engaged in a brutal battle for bottom-line profitability. The industry is navigating severe macroeconomic headwinds, driven by geopolitical instability, shifting consumer pricing expectations, and rising operational costs.

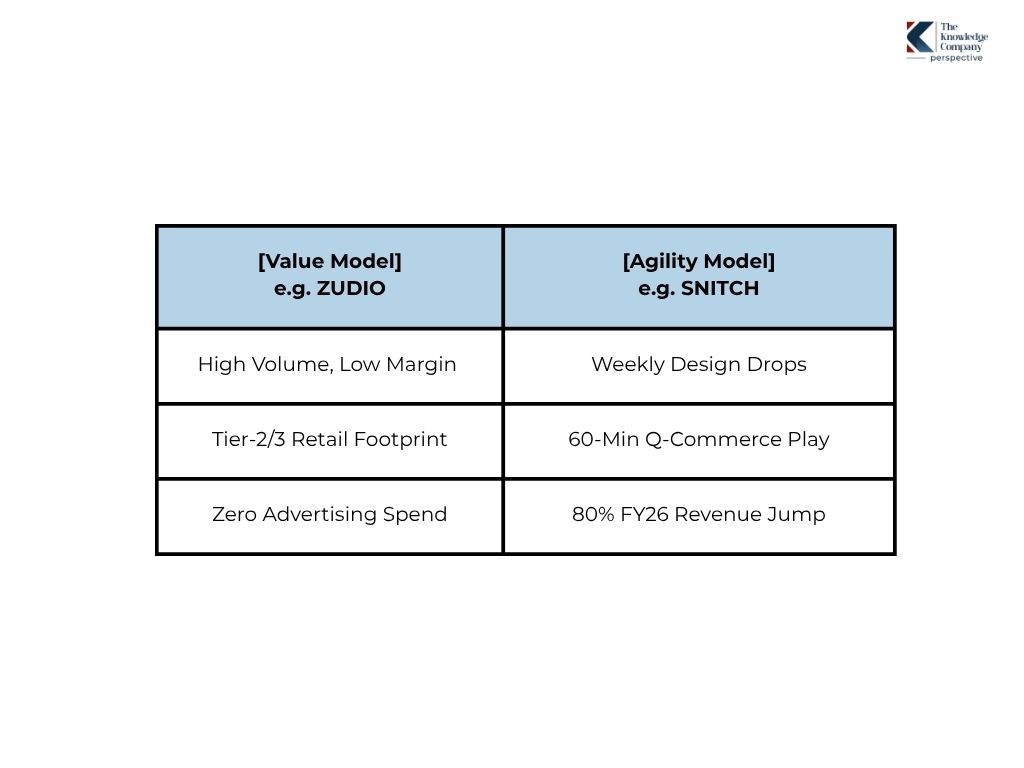

Comparative Operating Models: Value vs. Agility

To navigate these margin pressures, two distinct operating models have proven highly effective: the high-volume value model and the hyper-agile fast-fashion model.

Zudio (Tata Retail)

Operates on a hyper-scale, low-margin business model. By expanding aggressively into Tier-2 and Tier-3 cities and functioning as a high-traffic anchor tenant for commercial developers, Zudio drives massive profitability through sheer volume and zero-advertising strategies.

Snitch

Conversely, the D2C men’s fashion brand Snitch serves as a benchmark for hyper-agility. Snitch closed FY26 with a massive 80% jump in operating revenue to ₹900 crore (up from ₹498 crore in FY25), successfully reversing past net losses to hit an EBITDA profitability margin of 2–3%. Snitch operates in a “perpetual production mode,” dropping new styles weekly via a digitally native supply chain. Furthermore, the brand launched Snitch Quick, a 60-minute apparel delivery service across major cities (Bengaluru, Delhi, Gurugram) to capture instant Gen Z demand.

Influencer Power and the Tier 2/3 Phenomenon

Consumer discovery has been completely overhauled by the creator economy. Total influencer marketing spends in India have crossed ₹10,000 crore, with influencers acting as critical “performance infrastructure” that drives immediate, measurable conversions directly across digital commerce touchpoints. To combat ad-fraud, brands are deploying AI-powered data intelligence platforms to analyze creator profiles for authentic engagement.

Furthermore, the real momentum driving structural growth is stirring in “Bharat”—the regions beyond the Tier-1 metros (e.g., Indore, Lucknow, Surat, Bhubaneswar). Three out of every five new shoppers in India hail from these smaller geographies. Capturing this demographic requires hyper-localized marketing, deploying regional stars, and establishing decentralized regional warehouses that replenish fast-moving inventory daily to avoid margin-crushing inventory pileups.

Supply Chain Paradigm Shifts: Resilience, Tariffs, and Technology

The backend architecture of the Indian apparel industry is transitioning from a volume-driven, cost-focused model to a highly agile, technology-enabled ecosystem capable of withstanding severe geopolitical shocks.

The Geopolitics of Trade: The U.S. Tariff Shock

The fragility of India’s traditional textile supply chain was starkly exposed when the U.S. imposed a punitive 50% reciprocal tariff on Indian textile imports due to geopolitical alignments. Overnight, Indian cotton knits and denim became 30% more expensive than competing goods from Vietnam or Bangladesh, threatening up to 200,000 manufacturing jobs.

While a subsequent bilateral agreement successfully reset the tariff to a more manageable 18%, the crisis fundamentally altered the industry’s mindset. Indian manufacturers are now aggressively diversifying their export portfolios toward the European Union, Japan, and the Middle East to de-risk their books.

To survive compressed trend cycles under these tariff pressures, the supply chain is integrating AI and IoT. Indian manufacturers deploy predictive sourcing models, utilizing complex algorithms to analyze global weather patterns and geopolitical data to forecast raw cotton prices with near-perfect accuracy, successfully hedging against sudden raw material spikes.

PM MITRA Parks: The Infrastructure Mega-Push

To address systemic logistical inefficiencies and attract major foreign direct investment (FDI), the Government of India’s PM Mega Integrated Textile Region and Apparel (PM MITRA) scheme has shifted into hyper-drive. Backed by a budgetary outlay of ₹4,445 crore and a total project cost exceeding ₹13,040 crore ($1.44 billion), the scheme is actively setting up seven world-class integrated textile parks across the country.

The initiative has moved aggressively past blueprinting into execution:

These integrated hubs consolidate the entire textile value chain—from spinning and weaving to processing, garmenting, and printing—within a single plug-and-play ecosystem, systematically slashing logistics costs and compressed lead times.

Vision 2030 and Strategic Conclusion

The overarching roadmap for the Indian textile and apparel sector, encapsulated in Vision 2030, is defined by an aggressive pivot toward global dominance, technological superiority, and absolute sustainability. The Ministry of Textiles has set an ambitious target of $100 billion in textile exports by FY 2030–31, with a parallel aspiration to expand India’s share of global textile trade from roughly 4.7% to an aggressive 14–15%.

The urban and casualwear revolution unfolding in India signifies the structural and cultural evolution of the entire retail ecosystem. Brands that thrive in this era will be those that master extreme operational agility. They must simultaneously capture the hyper-fast, influencer-driven impulse buys of young consumers via 10-minute quick commerce platforms while catering to the sophisticated, specialized comfort demands of the growing Silver Economy. Supported by historic government infrastructure investments like the PM MITRA parks, predictive AI sourcing, and a relentless focus on sustainable design, India is systematically transitioning from a regional execution hub into a leading, innovation-led force in global fashion.